Mortgage Strategy Hub

Mortgage Strategies Most Buyers and Owners Never Hear Until It's Too Late

Whether you're buying your first home, moving up, or looking to refinance — these strategies will help you make a smarter move and keep more money in your pocket.

Want me to run your numbers? Book a call →

Zevi Shafran

President at Loan Brook, Inc. · NMLS #1067721

"This is exactly what I walk my clients through before they make a move. These aren't tips you'll find on a bank's website — they're the strategies that actually change the outcome. Find the section that matches what you commented, or scroll through all of them."

Start Here

Find the section that matches what you commented:

🏠 Buying a Home

📋 Costs & Fees

🔑 Owning & Refinancing

Buying a Home

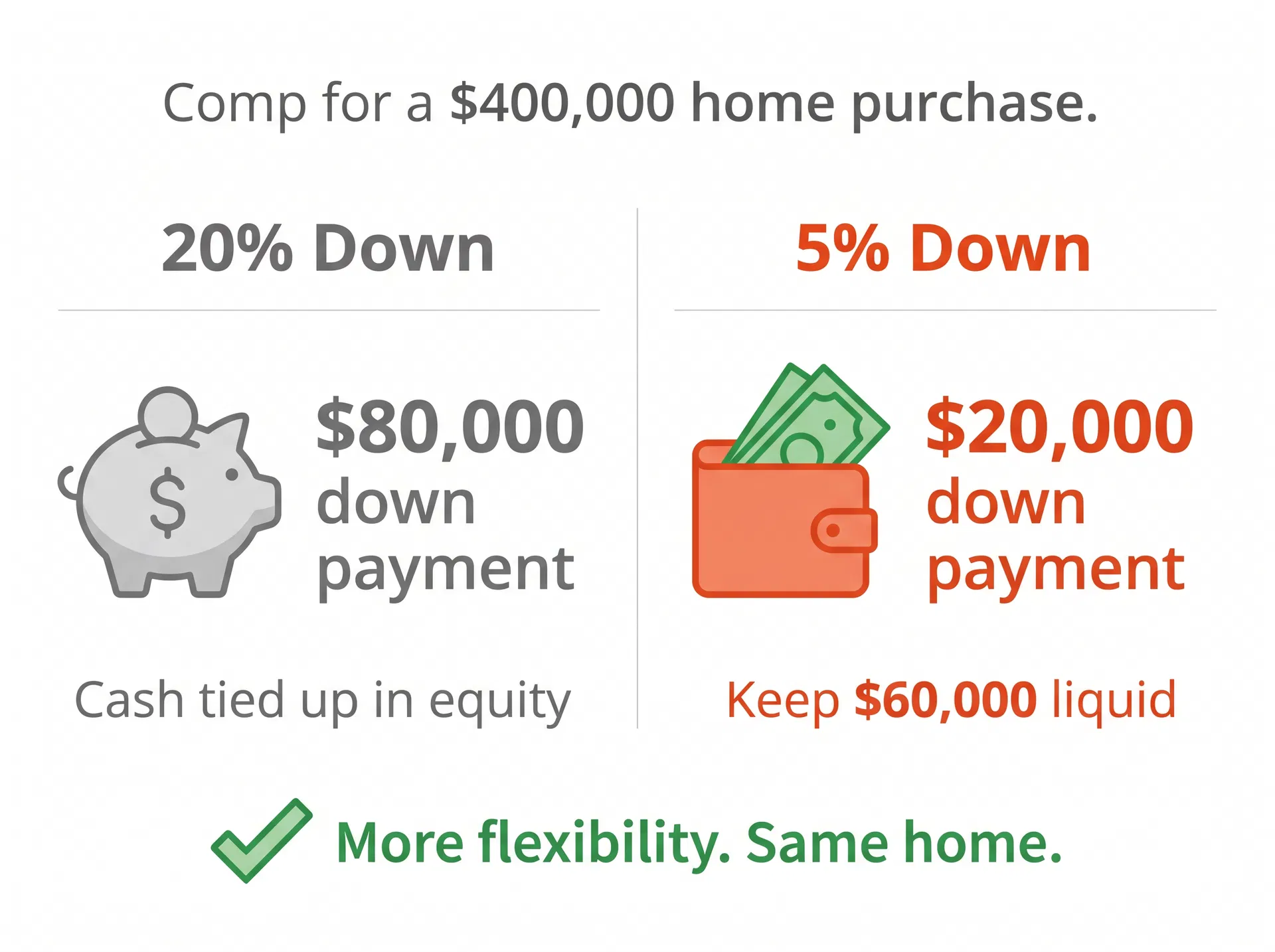

6 strategiesThe Down Payment Truth

The Mistake

Most buyers think they need 20% down to avoid mortgage insurance — so they drain their savings trying to get there.

The Reality

Putting 5% down and keeping the rest of your cash is usually the smarter move. There are strategies like Lender Paid Mortgage Insurance (LPMI) that let you avoid monthly PMI without putting 20% down. Your money stays liquid — available for emergencies, repairs, or investments.

What To Do

Ask your lender about LPMI and compare the total cost of 5% down vs. 20% down over 5 years — not just the monthly payment.

Quick Example

On a $400,000 home: 20% down = $80,000 out of pocket. 5% down = $20,000. That's $60,000 you keep in your pocket — working for you instead of sitting in your walls.

Want me to break this down for your situation?

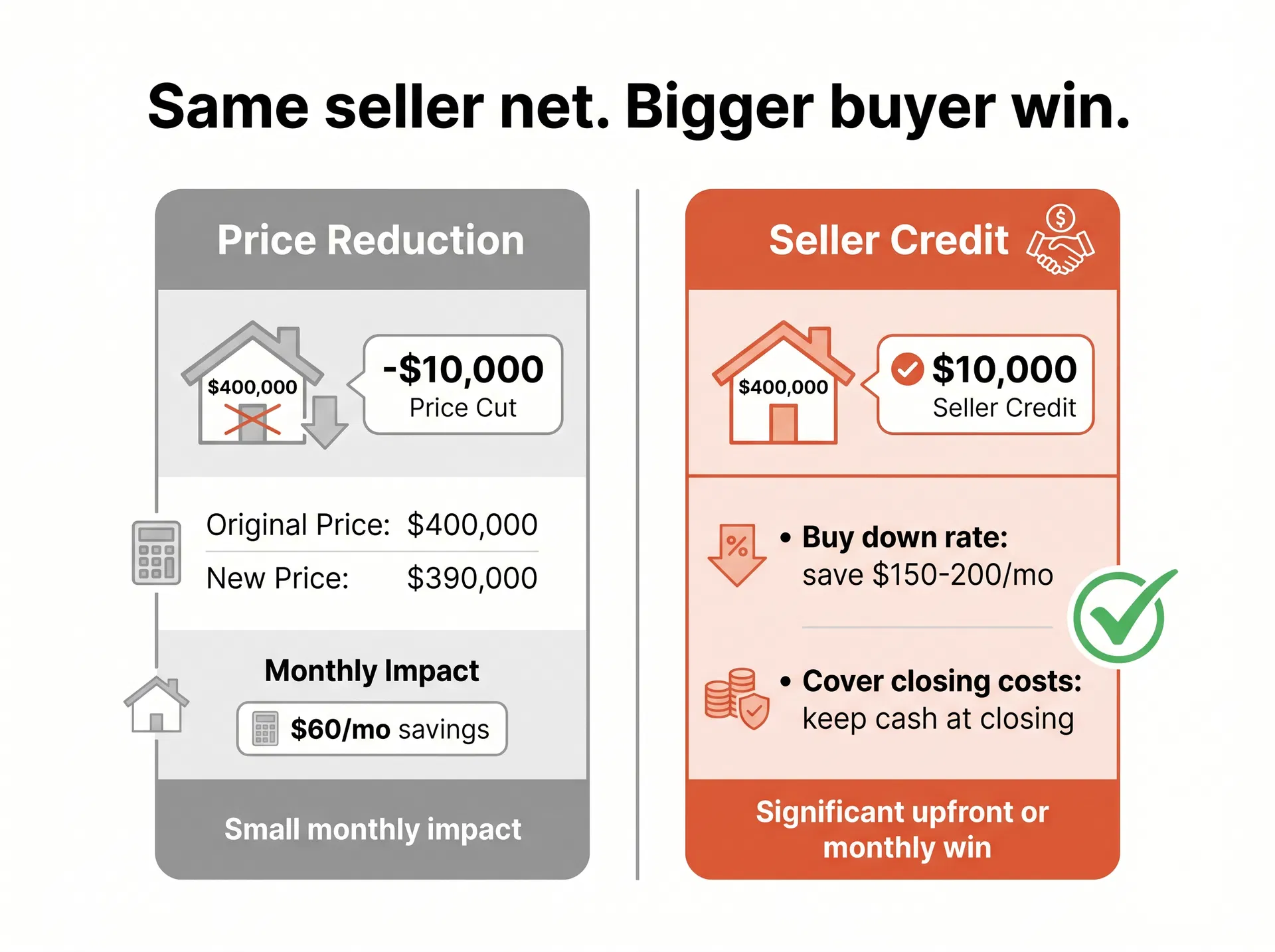

Book a Call →The Seller Credit Strategy

The Mistake

Buyers try to negotiate a lower purchase price to save money. A $10,000 price reduction only saves about $60/month on your mortgage.

The Reality

Instead of lowering the price, ask the seller for a credit. A $10,000 seller credit can permanently buy down your interest rate — saving you hundreds per month — or cover your closing costs so you bring less cash to the table. The seller nets the same amount. You win bigger.

What To Do

On your next offer, ask your agent to request a seller credit instead of (or in addition to) a price reduction. Then use that credit to buy down your rate.

Quick Example

On a $400,000 home: A $10,000 seller credit used to buy down the rate could save you $150–$200/month — vs. $60/month from a $10,000 price cut.

Want me to break this down for your situation?

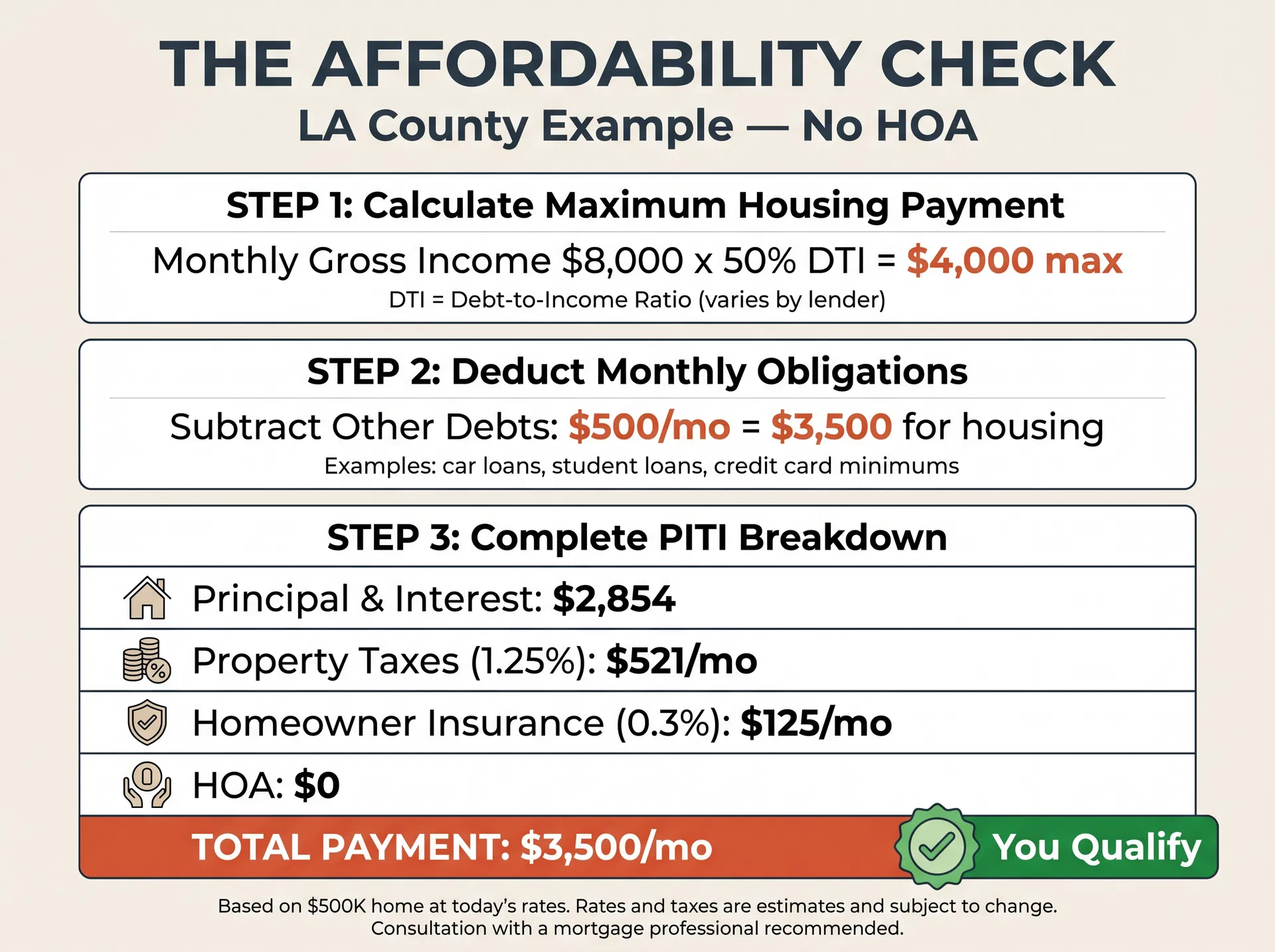

Book a Call →The Affordability Reality Check

The Mistake

People get pre-approved for a loan amount and assume that's what they can comfortably afford. The bank's max approval is not your budget.

The Reality

Lenders approve you based on Debt-to-Income ratio (DTI) — typically up to 50% of your gross monthly income. That total includes your full housing payment: principal & interest, property taxes, homeowner's insurance, and all other monthly debts. In LA County, property taxes run about 1.25% of the purchase price per year, and homeowner's insurance is typically around 0.3%. These alone can add $600–$800/month to your payment on a $400,000 home — and most buyers forget to account for them.

What To Do

Before you fall in love with a house, run this quick check: take your gross monthly income × 0.50, subtract all monthly debts. From what's left, subtract estimated taxes (purchase price × 1.25% ÷ 12) and insurance (purchase price × 0.3% ÷ 12). What remains is your max principal & interest payment.

Quick Example

$8,000/month gross income × 0.50 = $4,000 max DTI. Subtract $500 in car/debt payments = $3,500 for housing. On a $500,000 home: taxes ≈ $521/mo (1.25% ÷ 12), insurance ≈ $125/mo (0.3% ÷ 12). That leaves $2,854 for principal & interest — roughly a $430,000–$450,000 loan at today's rates. No HOA assumed.

Want me to break this down for your situation?

Book a Call →The 27-Year Mortgage Trick

The Mistake

Everyone defaults to a 30-year mortgage because the payment is lower. Most people don't know they have other options.

The Reality

You can ask your lender to structure your loan on a 27-year or 25-year term. The monthly payment increase is small — often less than $100/month. But you'll save tens of thousands in interest over the life of the loan and pay off your home years earlier. This applies to new purchases AND refinances.

What To Do

When you get your loan quote, ask your lender to show you the payment comparison for 30, 27, and 25-year terms. Then decide if the small payment bump is worth the long-term savings.

Quick Example

On a $350,000 loan at 7%: 30-year payment = $2,329/month. 27-year payment = $2,432/month. Difference = $103/month. Total interest savings = ~$28,000.

Want me to break this down for your situation?

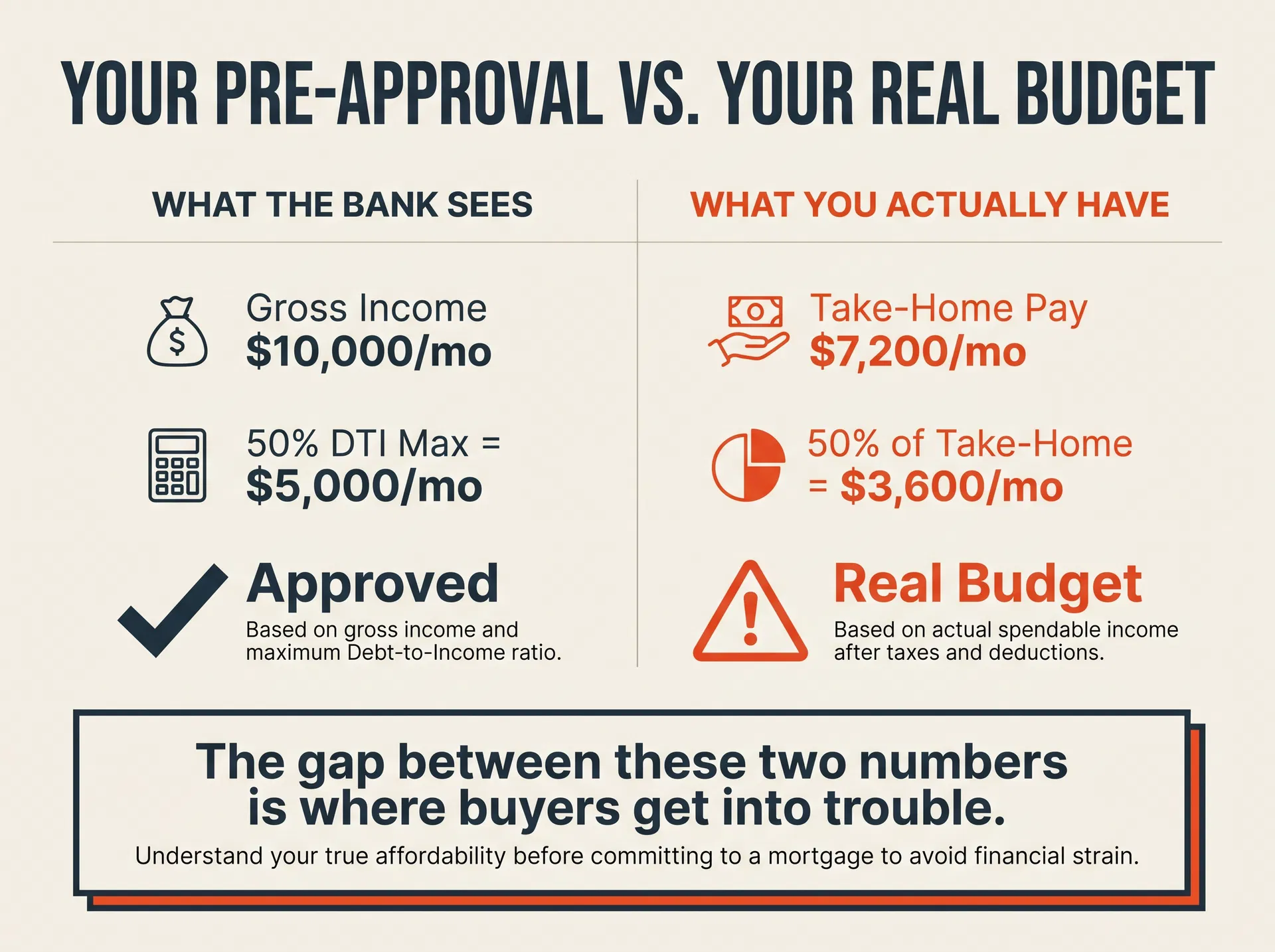

Book a Call →Your Pre-Approval vs. Your Real Budget

The Mistake

Buyers get pre-approved for a large loan amount and assume that's what they should be shopping at. The pre-approval number is the bank's max — not your comfortable budget.

The Reality

Your pre-approval is calculated on your gross income — before taxes, retirement contributions, or anything else comes out. But your mortgage payment comes out of your take-home pay. On a $10,000/month gross income, you might only take home $7,200. The bank approved you based on $10,000. Your pre-approval does factor in taxes, insurance, and HOA — but it uses estimates. If those estimates are too low, your actual payment could be hundreds more than what was modeled.

What To Do

Before you start shopping, calculate your comfortable payment based on your take-home pay — not your gross. A good rule: your total housing payment should feel manageable on your actual monthly bank deposit, not your pre-tax salary.

Quick Example

Gross income: $10,000/mo → Take-home: ~$7,200/mo. Bank approves up to $5,000/mo (50% DTI on gross). But 50% of your take-home is only $3,600/mo. The gap between those two numbers is where buyers get into financial trouble.

Want me to break this down for your situation?

Book a Call →The Gift Fund Loophole

The Mistake

First-time buyers don't know they can use gifted money for their down payment — or they try to use it incorrectly and get flagged at closing.

The Reality

You can use 100% gifted funds for your down payment on both Conventional and FHA loans — but only with the right documentation and timing. The lender requires a signed gift letter stating the funds are a gift, not a loan. If the lender thinks it's a loan, it counts as a debt and hurts your DTI. The money also needs to be seasoned — in your account for 60+ days before closing, depending on loan type.

What To Do

If family wants to help, move the money now — not two weeks before closing. Get a signed gift letter from the donor. Make sure your lender knows about it upfront so it's documented properly from the start.

Quick Example

Parents gift $40,000 for a down payment. With proper gift letter and 60-day seasoning, it's fully acceptable on a Conventional or FHA loan. Drop it in right before closing without documentation = lender flags it as an undisclosed liability.

Want me to break this down for your situation?

Book a Call →Costs & Fees

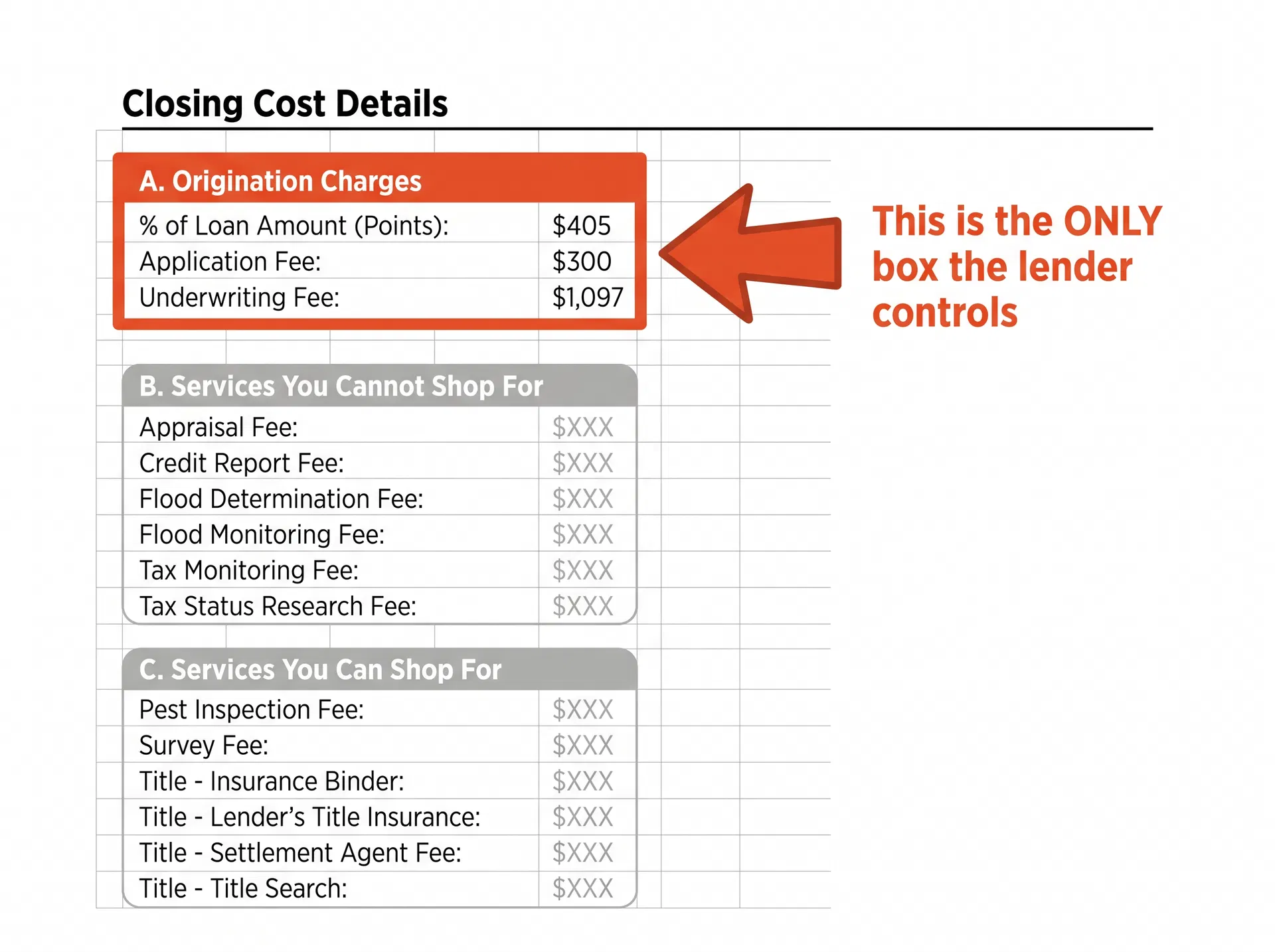

2 strategiesHow to Read a Loan Estimate

The Mistake

Most homebuyers get a Loan Estimate and either ignore it or get lost in three pages of taxes, title fees, and insurance numbers.

The Reality

You only need to look at one place: Page 2, Box A — Origination Charges. This is the only section the lender controls. Everything else (taxes, title, insurance) is roughly the same no matter which lender you choose. Box A is where lenders hide junk fees, inflated processing charges, and expensive discount points.

What To Do

When comparing lenders, pull up Page 2, Box A on each Loan Estimate. Add up the total. The lender with the lowest Box A total — at the same rate — is the better deal.

Quick Example

Lender A: Box A = $4,500. Lender B: Box A = $1,200. Same rate. Same loan. You just saved $3,300 by knowing where to look.

Want me to break this down for your situation?

Book a Call →The Rate Buy-Down Strategy

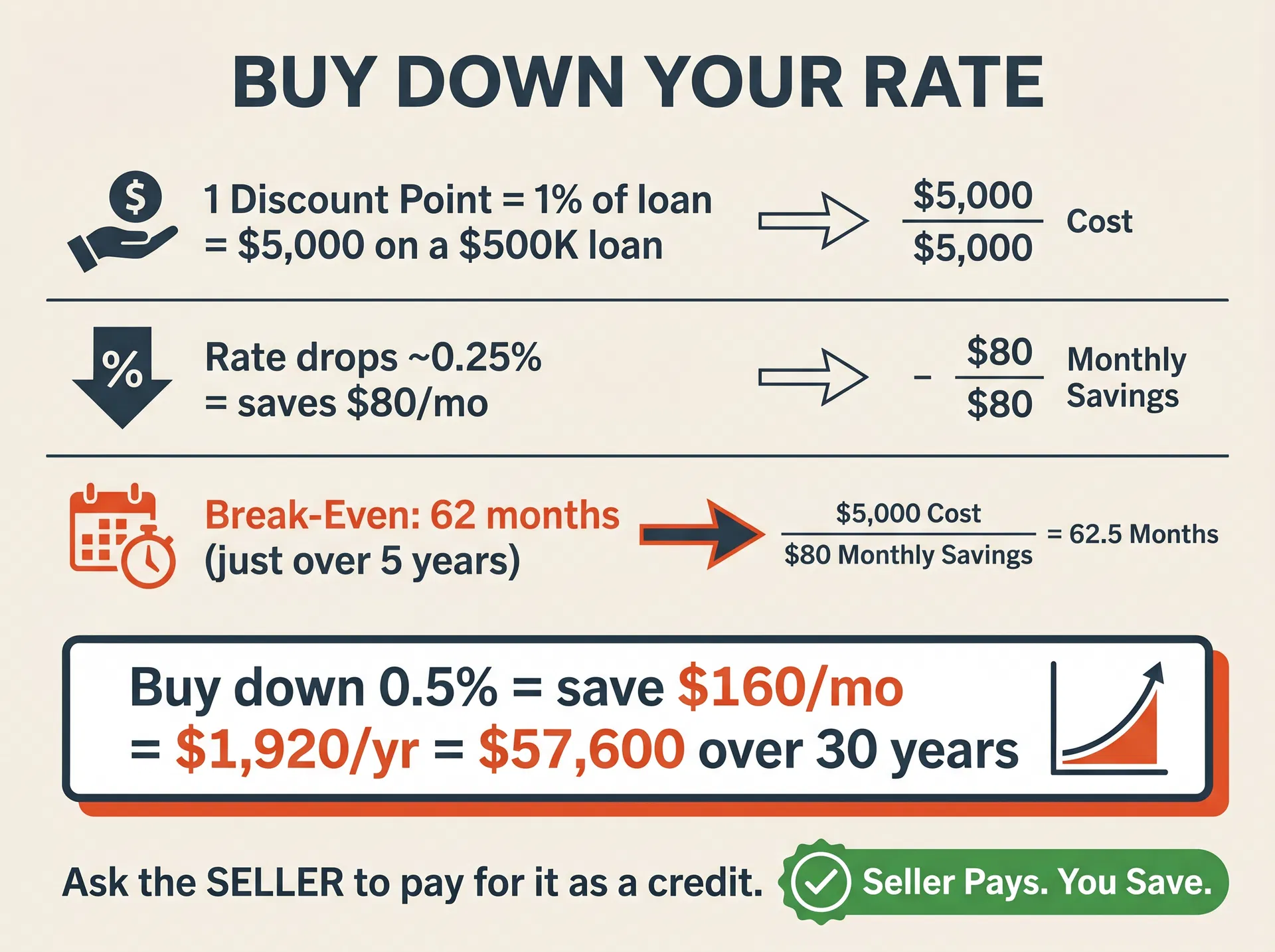

The Mistake

Most buyers just accept whatever interest rate their lender quotes them — not knowing they can buy it down, and that the seller can pay for it.

The Reality

One discount point costs 1% of your loan amount and typically lowers your rate by about 0.25%. On a $500,000 loan, one point = $5,000 and saves roughly $80/month. Your break-even is about 62 months. If you stay longer than that, you come out ahead. The key move: ask the seller to pay for the buy-down as a credit instead of (or in addition to) a price reduction.

What To Do

On your next offer, ask your agent to request a seller credit specifically to buy down your rate. Run the break-even calculation: closing cost ÷ monthly savings = months to break even. If you plan to stay past that point, it's a win.

Quick Example

$500K loan: buy down 0.5% = $10,000 cost, saves $160/mo = $1,920/yr = $57,600 over 30 years. Break-even: 62 months. Ask the seller to cover it — they net the same, you save for life.

Want me to break this down for your situation?

Book a Call →Owning & Refinancing

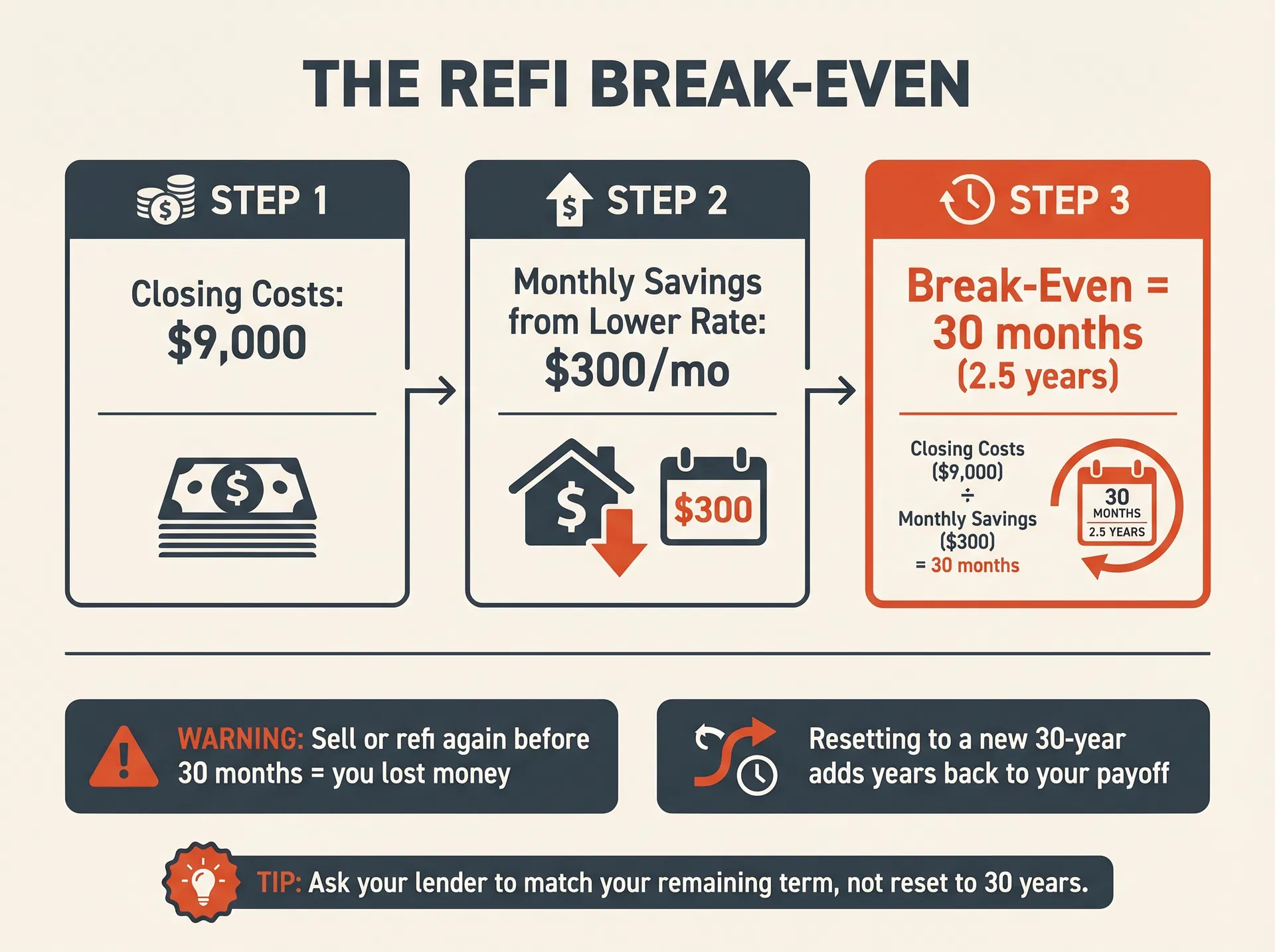

2 strategiesThe Refinance Trap

The Mistake

Homeowners refinance whenever rates drop without calculating whether it actually saves money. If you don't know your break-even point, you could lose money.

The Reality

Every refinance costs money — typically $8,000–$12,000 in closing costs on a $500K loan. Divide that by your monthly savings to find your break-even. If you sell or refinance again before hitting that point, you lost money. Worse: resetting to a new 30-year loan adds years back to your payoff date and restarts the interest-heavy early payment schedule.

What To Do

Before refinancing, calculate your break-even: closing costs ÷ monthly savings = months to break even. Ask your lender to match your remaining loan term — not reset to 30 years. Only refinance if the math works in your favor.

Quick Example

Closing costs: $9,000. Monthly savings: $300. Break-even = 30 months (2.5 years). If you sell before then, you lost money. Ask your lender to show you a 23-year refi if you have 23 years left — not a new 30.

Want me to break this down for your situation?

Book a Call →How to Remove PMI and Save Thousands

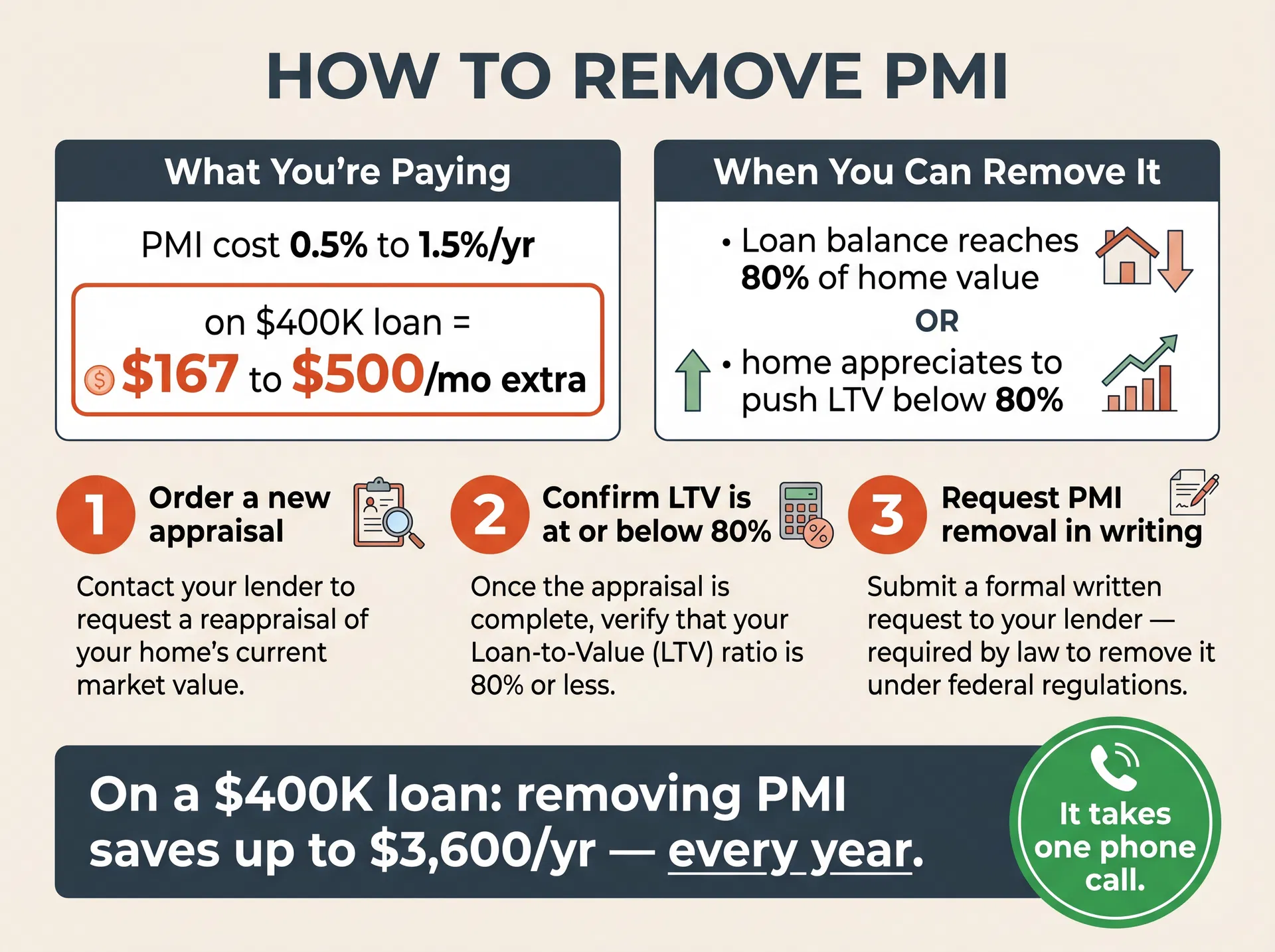

The Mistake

Homeowners who bought with less than 20% down keep paying PMI for years without realizing they may already qualify to remove it — especially if their home has appreciated.

The Reality

PMI costs 0.5%–1.5% of your loan per year. On a $400,000 loan that's $167–$500/month in extra cost. Once your loan balance reaches 80% of your home's value — either through payments or appreciation — you can request removal. Lenders are required by law to remove it when you ask and the LTV qualifies. A new appraisal may be all it takes.

What To Do

If you bought 2+ years ago, order a new appraisal. If your current home value puts your loan balance at or below 80% LTV, submit a written PMI removal request to your lender. They are legally required to remove it.

Quick Example

Bought a $400K home with 5% down in 2022. Home is now worth $480K. Loan balance: $365K. LTV = 76%. You qualify to remove PMI today. Savings: up to $3,600/year — every year.

Want me to break this down for your situation?

Book a Call →Quick Tool

Mortgage Payment Calculator

Estimate your monthly payment in seconds — whether you're buying or refinancing.

Estimated Monthly Payment

$2,728.56

P&I: $2,328.56 · Taxes: $300 · Insurance: $100

One More Thing

You probably only need one or two of these strategies.

But understanding all of them puts you in a position most buyers and owners never reach.

The difference between a good deal and a great deal is usually just knowing which question to ask — and when to ask it.

Want help figuring out what makes sense for your situation?

Book a Free Call — It's Free →Ready to Talk?

Book a Free 1-on-1 Call

Pick a time that works for you. We'll walk through your numbers, your options, and the best strategy for your situation — no pressure, no fluff.

This information is not a loan approval or commitment to lend. The actual loan amount, interest rate, fees, costs and monthly payment on your specific loan transaction can vary and will depend on your choice of loan product and your unique credit profile. Loans (in CA) will be made pursuant to DRE License #02001852 & NMLS License #1463667. Loan Brook, Inc. is an Equal Housing Loan Broker.

Copyright © 2026 Loan Brook, Inc. | All Rights Reserved